Award-winning contact centre, ready to help and right here in your community

Extensive network of branches for when you want to come and see us

Convenient, seamless digital banking, trusted by over 250,000 users

5 Star rated current accounts

Award-winning contact centre, ready to help and right here in your community

Extensive network of branches for when you want to come and see us

Convenient, seamless digital banking, trusted by over 250,000 users

5 Star rated current accounts

For their first pay rise negotiation!

Danske Discovery.

The fee-free bank account for growing ups aged 8-17.

10 x £1,000 to be won each month

We’ve already given our customers over £660,000.

Register now for a chance to win.

T&Cs apply.

We say YES to 9 out of 10 mortgage applications

A new home is closer than you think.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Applications subject to status and lending criteria. Approvals based on completed applications assessed from January to December 2025.

We're over the moon!

We’re thrilled to have been named a Which? Recommended Provider for our current accounts, highlighting our dedication to excellent service and quality products.

Personal banking that offers more

Bank your way

Manage your account online, over the phone or via video call, or come and see us in-branch.

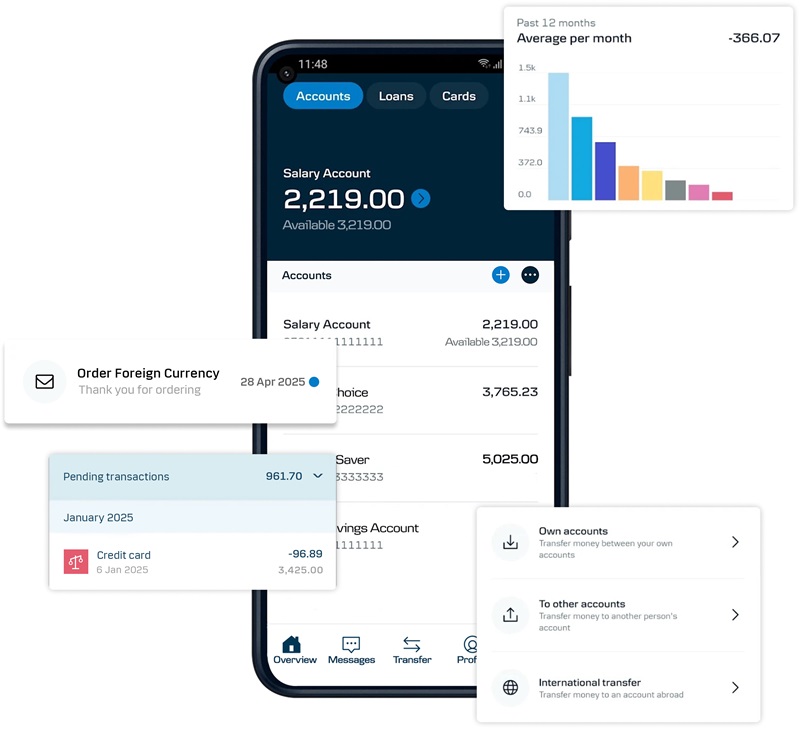

24/7 digital banking with eBanking and our mobile app – view spending, manage payments, chat to an adviser and more.

In the heart of your community, in person, at your local Branch, Post Office or Banking Hub.

By phone or video call, with our award winning contact centre.

Explore all ways to bank

Here to help

Reporting and fighting fraud

Find out how to identify and protect yourself from different types of frauds and scams, and how to report them.

Fraud and scams

Money worries

If you're concerned about the rising cost of living, or need help making repayments, we can help.

Visit money worries hub

Help going abroad

Card, cash or both? See how to use your Danske account if you’re travelling outside the UK.

Going abroad

Payments

Need help setting up one-off payments, Direct Debits or standing orders? Make it easy with eBanking.

Payments

Upload documents

If you’ve been asked to submit documents for proof of identity or address, or in advance of a meeting with us, you can...

Upload your documents

Savings calculator

Our clever calculator can help you work out how to reach your savings goals.

Use savings calculator

Supporting you through major life changes

Find more valuable support to help you manage your money throughout life's journey.

Visit support hubCustomer support

Looking for something specific? Here are our most popular shortcuts.

Chat to us

Here to talk

-

Mon–Fri: 8am–6pm / Sat: 9am–1pm / Sun: Closed

Mon–Fri: 8am–6pm / Sat: 9am–1pm / Sun: Closed

Chat with us

Here to take your questions

Start chatFind your nearest branch

Here to meet in person

Find branch details-

Existing Personal customer?

If you're an existing personal customer, you can contact us by phone or if you are registered for eBanking you can use our secure messaging service.

Send us a secure message via Secure Mail

Send message

eBanking and Mobile Banking Customer Support

NI/UK: 0345 603 1534

Outside NI/UK: +44 28 9004 9219

-

Mon–Fri: 8am–6pm / Sat & Sun: 9am–5pm

-

Independent service quality survey results

Personal Current Accounts

Published February 2026

As part of a regulatory requirement, an independent survey was conducted to ask customers of the 12 largest personal current account providers if they would recommend their provider to friends and family.

The results represent the view of customers who took part in the survey.

View all resultsPersonal Current Account Information

The Financial Conduct Authority requires us to publish the following information about our personal current accounts.

View information2024 Authorised Push Payment (APP) Scam Performance

Authorised push payment (APP) scams happen when someone is tricked into transferring money to a fraudster’s bank account. Information Danske Bank’s performance prior to the introduction of the reimbursement requirement in October 2024 can be found in PSR’s latest APP Scams Performance Report published in February 2026.

Latest stories

Danske Bank UK financial Results H1 2026

Read our financial results for the H1 of 2026.

View results

Danske Bank lowers age for Discovery Current Account to eight

Danske Bank has extended its Discovery Current Account to children aged 8 to 17, lowering the minimum age from 11. The bank has also removed fees on all accounts for customers under 18.

Read more

Alpha Housing secures £20m funding from Danske Bank to build 240 new homes

Alpha Housing has agreed a £20million sustainability-linked loan from Danske Bank to help deliver 240 new social homes across Northern Ireland over the next five years.

Read more