Helping Northern Ireland business thrive for over 200 years

Easy to use, customisable online banking

Dedicated local experts to support your business

*Source: MarketVue Business Banking from Savanta. YE Q1 2026 £0-1bn NI data. Data weighted by industry and turnover to be representative of NI businesses. Base: All exc Personal Banking = 928

Bank fee free when you're free.

2 years fee-free business banking with a Small Business Digital Account that works outside of 9 to 5. Just like you.

Available to businesses with a turnover of up to £1 million. Other terms and conditions apply.

Your business is our business

Right now, businesses with an annual turnover of over £1 million and borrowing requirements for £250,000 or more who switch to a Danske Large Business Account will benefit from:

- No valuation & legal fees

- No arrangement fees

- 75% off transaction fees and charges for 6 months

Terms and conditions apply.

'5 STAR' perfect!

We're star struck to have been awarded the 5* Moneyfacts product rating for our Small Business Digital Account, in recognition for the product's features, value and service.

We're here for you and your business

We know businesses come in all shapes and sizes, each with their own unique ambitions, priorities and goals. Whether you're a startup or an established business, our experts are here to help you thrive.

How we support you

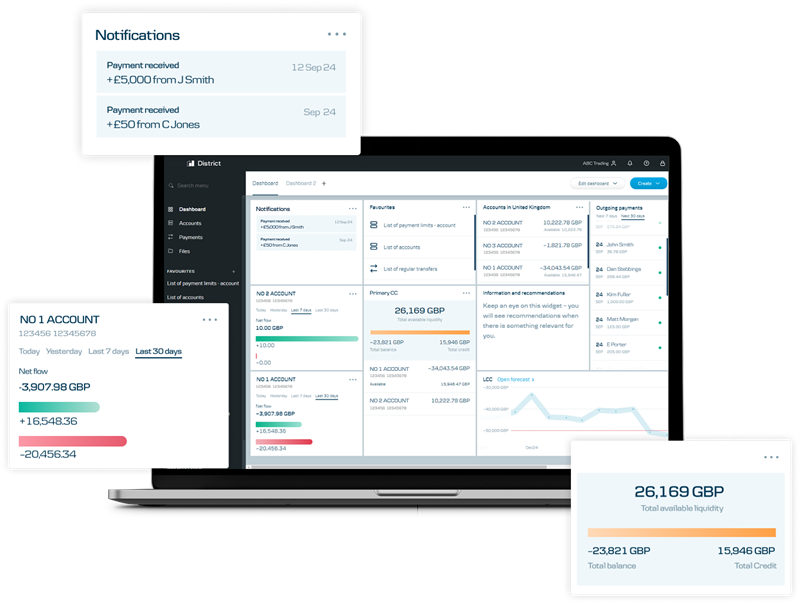

Online business banking

District is our online financial platform. Accessible online or on mobile via your browser, it provides a complete overview of your finances, no matter the complexity.

- Accessible. A single point of entry to your accounts, payments and liquidity.

- Insightful. Get support with your financial decision making.

- Integrated. Integration with most accountancy software platforms such as Xero, Quickbooks and FreeAgent with District.

- Customisable. You select the modules you require to assist you with your daily work.

- Controlled. Manage who uses your accounts and how they access them.

Our mobile and tablet business app allow you to create and authorise payments, view transaction history, send messages to your advisor and much more.

Explore District Explore Business AppsSupporting your business. Supporting you.

Sustainable finance

Sustainability is increasingly important to businesses and their customers. See how we can support you on your journey to a more sustainable future.

Sustainable future

Rising cost of doing business

We know that operating costs are soaring for many businesses. If you’re starting to feel the impact, please get in touch as we may be able to help.

Rising business costs

Frauds and Scams

With fraud and scams becoming more sophisticated, check out the latest resources to help protect you and your business from financial attacks.

Help protect your business

Government schemes

Several schemes were set up to provide support during and after the pandemic. Find out more about them, plus the Pay as you Grow options.

View Pay as you GrowExplore all schemes

Danske Economic Hub

Insights and forecasts from our local Economist Team including quarterly sectoral forecasts and consumer confidence reports.

Explore Danske Economic Hub

“

Danske’s online banking system has been invaluable – it is easy to use and has a range of features that helps us manage our cash flow.”

Ashleigh Averell, ibrand Everything Ltd, Newtownabbey

“

Danske Bank's local decision-making was key in helping us transform our plans into reality. Danske have supported our growth plans and understand our daily operations and future aspirations.”

Finlay Robinson, Robinson’s Supermarket, Ballymena

“

The team at Danske Bank took time to understand our growth ambitions and how they could help us on our exciting future plans. The support and lending facilities provided by Danske has been a key part of our expansion.”

Pauline McKeating, Mercedes Benz NI Truck and Van, Dungannon

Independent service quality survey results

Business Current Accounts

Published February 2026

As part of a regulatory requirement, an independent survey was conducted to ask customers of the 5 largest business current account providers if they would recommend their provider to other small and medium enterprises (SMEs).

The results represent the view of customers who took part in the survey.

View all results

Information about business current account services

We’re required by the Financial Conduct Authority to publish information about our business current account services.

This includes, amongst other things:

- How to open a current account with us, and what you'll need to do;

- How and when you can contact us if you have a question of concern

Explore finance options

Small Business Borrowing

The information contained in this page is primarily aimed at those customers interested in borrowing up to £25,000.

Borrowing information

Alternative Finance Options

When we aren’t in a position to provide funding we would still like to help by providing some other potential funding sources.

Explore potential funding

Trade Finance

We have a range of products that can help minimise credit risks and manage credit terms and payment flows for buyers.

View product rangeWe're here to help

Here to talk

-

Mon–Fri: 8am–6pm / Sat: 9am–1pm / Sun: Closed

Mon–Fri: 8am–6pm / Sat: 9am–1pm / Sun: Closed

Use start chat button to begin

Here to take your questions

Start chatFind your nearest branch

Here to meet in person

Find branch details-

Existing business customer?

If you're an existing business customer, you can contact us by phone or if you are registered for District you can use our secure messaging service.

Send us a secure message via our online platform, District

Send message

District Customer Support

NI/UK: 028 9031 1377

Outside NI/UK: +4428 9031 1377

-

Mon–Fri: 8am–5pm / Weekends: Closed

Mon–Fri: 8am–5pm / Weekends: Closed

-